A lot has changed since President Obama signed the Patient Protection and Affordable Care Act on March 23, 2010. Back then, we were still a few weeks away from finding out what this “iPad” gadget was all about; the Giants had never won a World Series in San Francisco; we still knew Miley Cyrus as Hannah Montana.

And now five years, 200 million iPads, 3 World Series victories, and countless headlines of Miley just being Miley later, we are still waiting for the Affordable Care Act, or ACA, to fully take effect.

Which actually isn’t terribly surprising, since the US healthcare system accounts for almost 20% of our economy each year. That’s $3 trillion dollars. 12 zeros. And since the ACA’s scope was intended as a total reform of this gigantic industry—including federal and state regulators, providers, payors, patients—5 years doesn’t seem that long of a time.

After all, chaos would ensue if it had just come in like a wrecking ball.

So as we celebrate the 5-year anniversary of its signing, let’s take a quick look back at all that has happened, all that will, and what it means to those affected.

Progress Thus Far

Some mandates of the ACA went into effect immediately in 2010:

- Dependent children can be covered on a parental plan up to age 26

- No lifetime dollar limits on coverage

- No cost sharing for preventive care

Some took a little longer:

- In 2012, health insurers had to abide by new Medical Loss Ratio standards, which dictates the percentage of money insurers must spend on improving the health care of their members (typically through claims payments)

Others just recently went into effect in 2014:

- The Individual Mandate went live, requiring all individuals to carry health insurance.

- Healthcare exchanges came online, allowing people to shop for and purchase individual insurance

The Shape of Things to Come

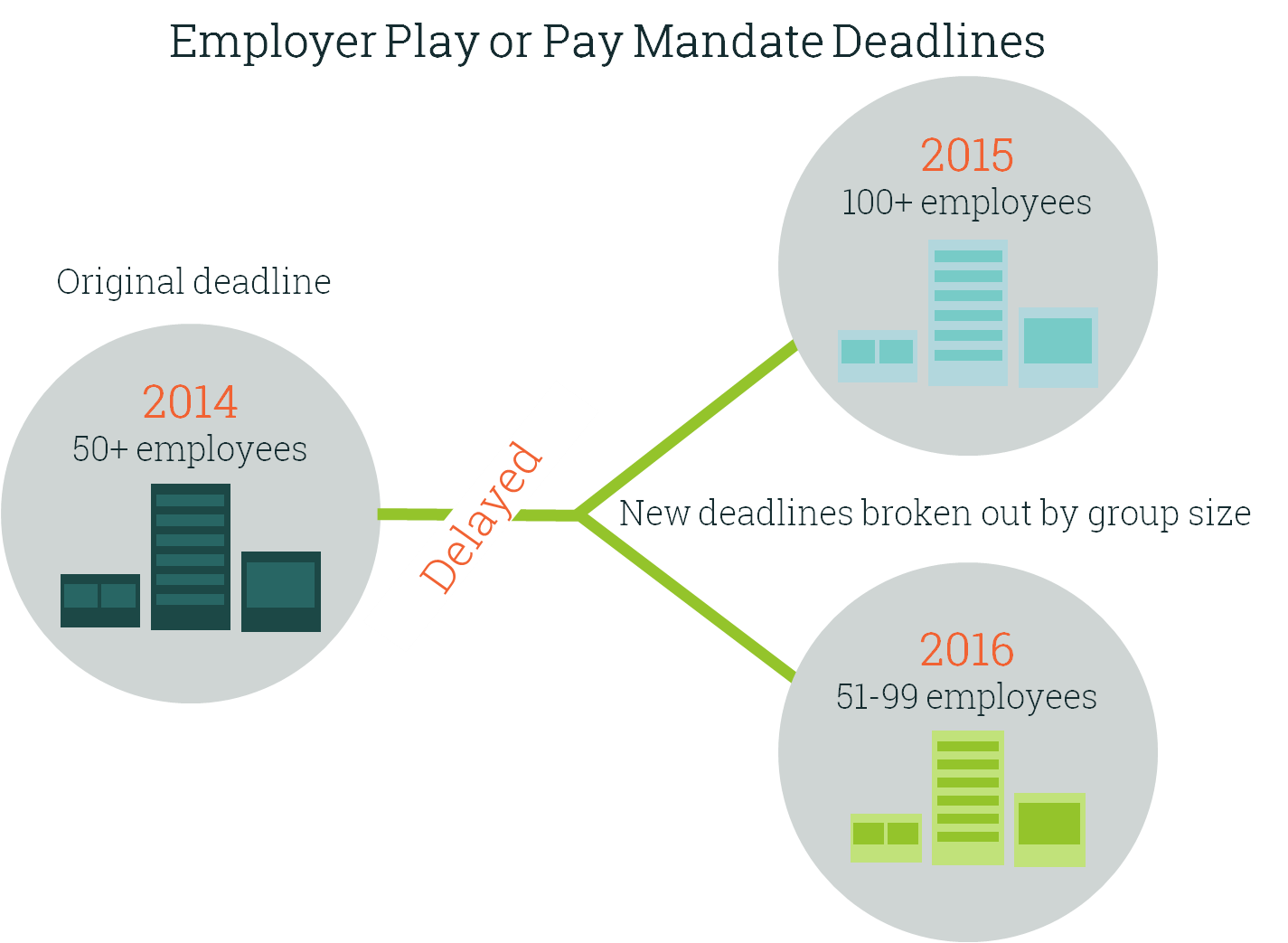

Many other provisions of the ACA, especially those that most affect businesses under 100 employees, have been delayed, and here is where it gets tricky(er).

The Small Business Health Option Program (SHOP) was delayed in many states (although not in California where Covered California has been available since January 2014), along with the Employer Play or Pay Mandate that requires certain businesses to offer health insurance coverage to their employees.

Small Groups

For California groups with less than 50 employees who had coverage in 2013, they were allowed to “early renew” their plans on December 1, 2013 and “grandfather” themselves into their existing plans to avoid moving to ACA-compliant plans until the end of 2014. Then in 2014, “early renewal” was offered again by a different ancestor, and groups were allowed to “grandmother” themselves into their existing plans one more time.

And unless we all of a sudden find ourselves with an estranged great-granduncle (which isn’t to say is impossible—family trees, as with major reform implementations, can yield surprises), there will be no more extensions for groups with under 50 employees.

Bigger Small Groups

Also coming down the pipeline in 2016 is one of the largest changes for groups under 100 employees. Currently, the small group market is defined as companies with 2-50 employees. Beginning January 1, 2016, the classification of a “small group” will expand to include all companies with 2-100 employees.

So five years in the making, moving to ACA-compliant plans will finally be a reality. Plan benefits may become poorer. Costs will likely increase. Also, rate structures will become age banded and community rated, posing unique administrative challenges.

What Now?

But not all is doom and gloom, and there are options to minimize the impact of these changes and maintain control of benefits programs as companies come up on their 2015 and 2016 renewals:

Option 1: Leverage a Pooling Model

- PEOs and trusts provide price control and stability, as well as typically richer benefits, which are not usually available to small companies. These products pool many small groups together so they have “big company” leverage.

- Be careful, though: joining a poor quality pool could add risk and cost uncertainty.

Option 2: Wait for more delays

- While all indications show that these changes will go in to effect, the history of implementation has proven that anything is possible.

- Especially for groups with 2-50 employees, it looks like the delays have run their course. 51-99 groups, though, will likely have a chance to “early renew” their plans for December 1, 2015 so that they can stay on the large group platform until their 2016 renewal.

- Any further procrastination is just delaying the inevitable. Whether it is 2015 or 2016 or 2017, all companies will eventually be forced to change to ACA-compliant plans.

Option 3: Move to a self-insured or partially self-insured model

- Companies under 100 do not normally think of self-insurance as a potential solution, but there are a number of options available that allow for smaller companies to self-insure.

- Potential cost volatility, increased risk, and increased administrative burdens, however, could mean that this is not a good fit for some small companies.

Option 4: Move to an ACA plan

- While ACA-compliant plans certainly come with their challenges, they are still a viable option to offer coverage to employees.

- Companies with higher risk factors like an older population or employees with serious ongoing medical conditions benefit from community rating.

So now, five years after it was first signed into existence, the ACA’s full presence is slowly reverberating across America, and while the uncertainty of the next five years can seem scary, just think back to 2010. Who (but Apple) knew that we would embrace tablet computing the way we did? Who (but the Giants) believed that we could see them parade down Market Street three times in just about as many years?

So much is possible with the right knowledge about the best choices, and we can help with that. If you are interested in learning more about any of the options we described above, or have not yet decided which option is best for you, contact one of our expert consultants today to start a conversation: info@sequoia.com.

We’ll make it feel like a party in the USA.

P.S. For further reading, check out our deep dive into alternatives to ACA plans for small businesses.