In the past twelve months, we have seen directors and officers liability rates increase, capacities drop, and appetites change. Underwriters are being very conservative in their approach to quote even renewal business, and are simultaneously increasing premiums and narrowing coverage.

As the financial impact of the pandemic continues, here is what you can expect in respect to directors and officers (D&O) insurance at both private and public companies.

Private Company D&O

Private company D&O is, by nature, broader in coverage than public company D&O. Unlike public company coverage, private D&O generally includes entity coverage and can be bundled with employment practices liability insurance (EPLI).

As COVID-19 spread in 2020, many markets stopped writing new business altogether, afraid of the impact that furloughs and layoffs would have under the EPLI coverage. In respect to renewals, if they did not non-renew, underwriters increased retentions (oftentimes by more than double), increased premiums, and quoted more restrictive coverage.

As the pandemic continued, underwriters once again started reconsidering new accounts, but with newer, more stringent requirements. For example, they require a full financial picture, wanting information on everything, from an organizations’ relationships with debt holders, to how COVID-19 is affecting their businesses.

The primary concern for underwriters is a company’s financial health and its ability to navigate the pandemic. The want some security that these organizations will remain financially viable for the next 12 to 18 months. If underwriters do not get answers to all their questions or if answers do not meet their standards, they will likely reject the application. As renewals come up, you should prepare yourself for a few realities:

- Rate increase – expect increase of 10-25%.

- Higher retentions – expect retentions to potentially double.

- Restrictive coverage – expect changes in terms and conditions, typically not in a favorable way.

The following D&O exclusions are also becoming more common:

- Bankruptcy – in today’s unstable economy, underwriters are not taking any chances on potential litigation because of bankruptcy.

- Creditors – like bankruptcy, litigation from creditors are another concern for underwriters.

- Infectious diseases – COVID-19 may be at the root of their worries, but underwriters are trying to encompass any other sort of infections that may trigger litigation under this exclusion.

Going forward, we need a proactive approach:

- Partner with your broker as early as possible. With the current state of the marketplace, you do not want to rush. Underwriters are receiving a high volume of submissions and there is a significant delay in getting quotes.

- Prioritize coverage. The value of a D&O policy lies in its terms and conditions. Yes, cash may be king, but in these unprecedented times you want to be sure that the coverage is there should litigation occur. Therefore, if you have options, prioritize coverage over premium.

- Communicate. Submit complete applications with full details. This will not only give underwriters a deeper understanding of your business, but potentially avoid further delays due to an incomplete submission.

- Be flexible. You may achieve better results with flexibility and creativity. Talk to your broker about your expectations. If saving premium dollars is a priority, your broker may be able to find creative alternatives to help achieve it via a higher retention or a specific exclusion.

Public Company D&O

Similar to private company D&O, public company D&O has also been affected by the pandemic, but there are different dynamics at play. For one, public companies’ financials are closely watched by customers, creditors, and investors, all of whom are potential claimants.

Typical loss drivers for public companies include securities claims, cyber events, bankruptcy, issues around mergers and acquisition, and now, they also include COVID-19. Like underwriters in the private D&O space, public company underwriters are also interested in financial health, often requiring audited financials for their review, as well as pandemic questionnaires.

Capacity is now limited, meaning that building a coverage tower is not as easy as in prior years. Carriers are not offering $10 million limits. Instead, most are not going higher than $5 million or even $2.5 million. Self-insured retentions are at a minimum of $1 million. Additionally, premiums are up 30% to 40% from last year.

Exclusions for coverage are getting also broader. Carriers are limiting coverage or adding higher retentions for claims alleging antitrust. Others are completely excluding antitrust, or expanding the exclusion to apply to claims alleging anticompetitive behavior, instead of just the usual violation of federal antitrust laws.

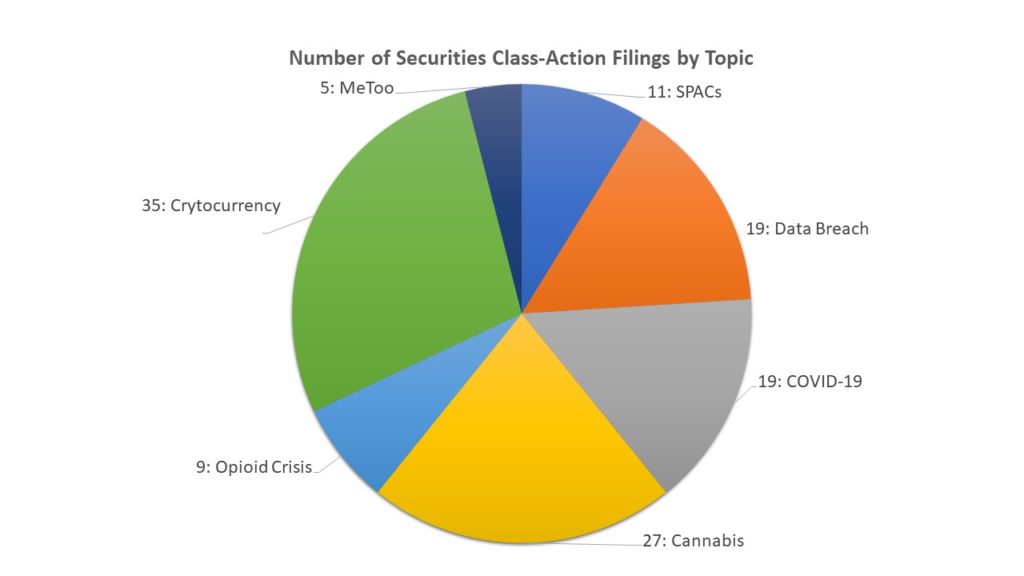

Additionally, securities class-actions lawsuits remain a risk. As of January 2021, the leading causes for these claims were: cryptocurrency, cannabis, data breach, COVID-19 and SPACS. A visual of this was provided by the Securities Class Action Clearinghouse, maintained by Stanford Law School and Cornerstone Research:

Conclusion

The current state of the market may be a sticker shock for many. In the foreseeable future, we expect rates to continue to increase, retentions to double and restrictive coverage to remain in place for private and public companies alike.

While 2021’s market may begin to stabilize, it is unlikely for it to return to a pre-2019 state. Our recommendation is to partner with your broker as early as possible. Communicate with them and make sure they set expectations for a successful renewal per today’s standards. Be ready to provide details, be transparent, and lastly, be flexible. To read the full article with updates, please click here.

To discuss your upcoming D&O renewal, please contact your Sequoia Risk Advisor or connect with them directly in HRX.

Disclaimer: This content is intended for informational purposes only and should not be construed as legal, medical or tax advice. It provides general information and is not intended to encompass all compliance and legal obligations that may be applicable. This information and any questions as to your specific circumstances should be reviewed with your respective legal counsel and/or tax advisor as we do not provide legal or tax advice. Please note that this information may be subject to change based on legislative changes. © 2021 Sequoia Benefits & Insurance Services, LLC. All Rights Reserved